Your Trusted Partner in Real Estate. Contact me at 403-990-7990 for all your property needs.

Real Estate

NEWSLETTER

|

Detached

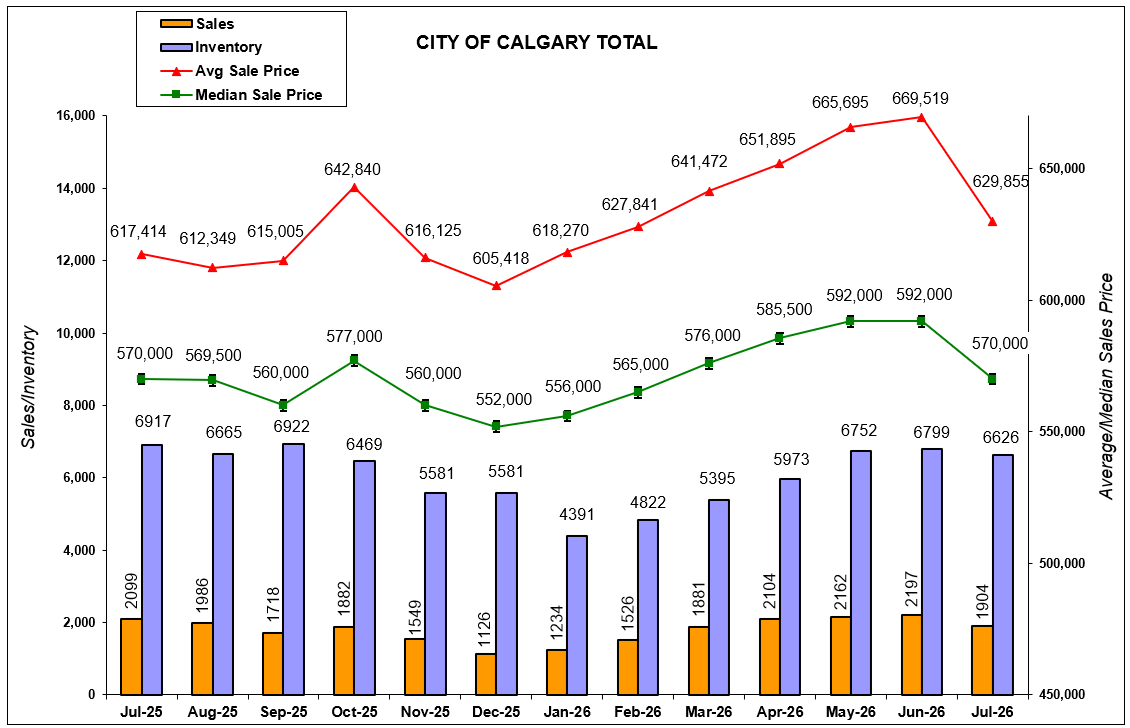

Calgary's detached housing market remained balanced in July despite slower activity. Sales declined nearly 2% year-over-year to 1,012 units, while new listings fell 9%, keeping inventory below last year's levels. Months of supply increased to nearly three months, ranging from under two months in the West District to over five months in the North East. The benchmark detached home price eased to $743,900, down nearly 2% from last July. Prices remain well above pre-2024 levels, although trends vary by district. City Centre and the West posted annual gains, while the North East recorded the largest decline at nearly 6%.

Semi-Detached

Calgary's semi-detached market remained balanced in July. Sales were in line with last year, keeping year-to-date activity consistent with 2025. Although new listings declined in July, supply remains relatively tight, with a sales-to-new-listings ratio near 60% and less than three months of inventory. The benchmark price was $691,000, down slightly from June but unchanged from last year. Prices have remained stable overall, though market conditions vary by district. The West District posted the only year-over-year price gain, while the North East shifted into buyers' market conditions with the largest price declines.

Row

Calgary's row home market continued to slow in July, with sales declining for the third consecutive month and year-to-date sales down 15%. New listings have also eased, keeping the sales-to-new-listings ratio above 55%, but inventory remains elevated compared with long-term trends. Slower sales pushed the months of supply to close to 4, limiting further price growth. The benchmark price declined to $418,500, down from June and 6% below last year’s level. Increased competition from new home construction continues to pressure resale row home prices.

Apartment

Calgary's resale apartment market continues to favour buyers as increased rental options and new supply weigh on ownership demand. Sales are down nearly 26% year-to-date, while elevated inventory levels continue to pressure the market despite fewer new listings. With nearly 2,000 units available for resale, months of supply remain high, limiting price growth. The benchmark apartment price declined to $297,600 in July, down over 8% from last year and 13% below the 2024 peak. Price declines have been widespread across all districts. |

The average number of days on the market (Calgary Metro)

Average days on the market in July 2026 | Average days on the market in July 2025 | |

Detached | 33 | 34 |

Apartment | 54 | 45 |

Semi-detached | 36 | 34 |

Row | 44 | 37 |

Median price (Calgary Metro)

Median price in July 2026 | Median price in July 2025 | Percentage change | |

Detached | $688,500 | $705,000 | -2% |

Apartment | $290,000 | $310,000 | -6% |

| Semi-Detached | $567,500 | $605,000 | -6% |

Row | $403,000 | $434,900 | -7% |

The median price is where half sell for more and half for less.

Months of supply (Calgary Metro)

| January 2023 | 2.04 |

| February 2023 | 1.58 |

| March 2023 | 1.33 |

| April 2023 | 1.20 |

| May 2023 | 1.03 |

| June 2023 | 1.10 |

| July 2023 | 1.32 |

| August 2023 | 1.19 |

| September 2023 | 1.38 |

| October 2023 | 1.47 |

| November 2023 | 1.67 |

| December 2023 | 1.34 |

| January 2024 | 1.30 |

| February 2024 | 1.10 |

| March 2024 | 0.95 |

| April 2024 | 0.94 |

| May 2024 | 1.10 |

| June 2024 | 1.38 |

| July 2024 | 1.75 |

| August 2024 | 2.05 |

| September 2024 | 2.53 |

| October 2024 | 2.28 |

| November 2024 | 2.42 |

| December 2024 | 2.26 |

| January 2025 | 2.51 |

| February 2025 | 2.41 |

| March 2025 | 2.39 |

| April 2025 | 2.62 |

| May 2025 | 2.62 |

| June 2025 | 3.04 |

| July 2025 | 3.30 |

| August 2025 | 3.35 |

| September 2025 | 4.02 |

| October 2025 | 3.43 |

| November 2025 | 3.59 |

| December | 3.43 |

| January 2026 | 3.56 |

| February 2026 | 3.16 |

| March 2026 | 2.87 |

| April 2026 | 2.84 |

| May 2026 | 3.12 |

| June 2026 | 3.09 |

| July 2026 | 3.48 |

Source: Calgary Real Estate Board

Calgary Metro-within Calgary City Limits

Your Trusted Partner in Real Estate. Contact me at 403-990-7990 for all your property needs.

Cell: 403-990-7990

{phone_2_label}: {phone_2}

info@homeguy.ca

Head Office

320-180 Quarry Park Blvd SE

Calgary, AB, T2C 3G3